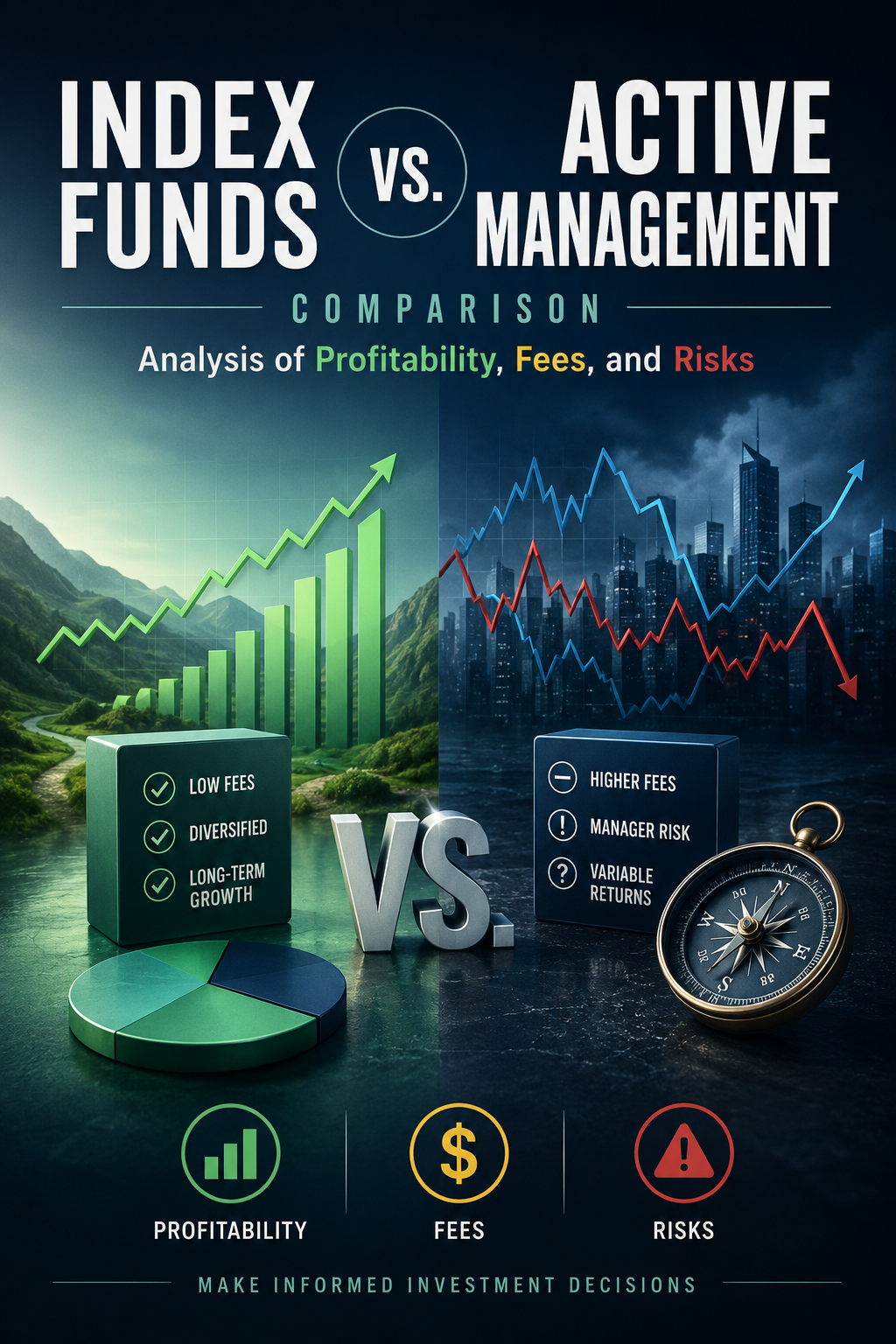

The decision on how to structure a long-term portfolio usually centers on one of the most persistent debates in the financial sphere: the index funds vs. active management comparison. Both approaches are based on opposing theoretical premises regarding market efficiency and offer completely different fee structures, risk profiles, and asset selection methodologies.

The objective of this analysis is to break down, objectively and based on data, how both investment vehicles operate, the impact of structural costs (TER) over the long term, and how they approach risk management.

What are Active Management Funds?

Active management is based on the premise that financial markets present inefficiencies that can be exploited. In this model, a professional manager or a team of analysts makes discretionary decisions about which assets to buy, hold, or sell.

The main objective of an actively managed fund is to generate «Alpha», meaning to achieve a return superior to its benchmark index while assuming a controlled level of risk. To achieve this, management teams use various methodologies:

- Fundamental Analysis: Evaluation of financial statements, cash flows, and competitive advantages of companies.

- Macroeconomic Analysis (Top-Down): Study of global variables such as interest rates, inflation, and economic growth to determine the most favorable sectors.

- Quantitative Analysis: Use of mathematical models and algorithms to identify price patterns.

What are Index Funds (Passive Management)?

Conversely, index funds (and ETFs that track indices) are rooted in the Efficient Market Hypothesis (EMH). This theory suggests that asset prices already reflect all available public information, making it statistically unlikely to consistently beat the market once costs are deducted.

An index fund does not seek to beat the market, but rather to replicate its performance. Its goal is to generate a return equal to a specific index (such as the S&P 500, MSCI World, or IBEX 35), minimizing the Tracking Error (the deviation from the index).

Profitability Analysis: Empirical Data and SPIVA Studies

When evaluating the index funds vs. active management comparison, historical profitability is one of the most studied factors. It is essential to remember that past performance does not guarantee future returns, but historical data offers clear context on the behavior of both models.

The SPIVA (S&P Indices Versus Active) reports, produced by S&P Dow Jones Indices, are the industry standard for measuring the performance of active managers against their respective indices. Historically, these reports have shown a consistent trend over extended time horizons (10 or 15 years):

- Difficulty of outperformance in the long term: In most developed markets (especially U.S. large-cap equity), a high percentage of actively managed funds fail to beat their benchmark over periods exceeding a decade.

- Inefficient markets: Active managers often argue that they have a higher probability of generating Alpha in less efficient or less analyzed markets, such as emerging markets or small-cap companies.

- Performance persistence: Funds that manage to position themselves in the top quartile of performance over a 5-year period rarely manage to remain in that same quartile over the following 5 years.

The Impact of Fees (TER) in the Long Term

One of the most quantifiable differences in this comparison is the cost structure. The TER (Total Expense Ratio) encompasses management fees, depository fees, and other operational expenses.

| Cost Characteristic | Active Management | Index Funds |

| Management Fee | Generally high (0.75% – 2.00% annually), intended to pay the analysis and management team. | Very low (0.05% – 0.30% annually), as the process is largely automated. |

| Transaction Costs | High. Portfolio turnover implies higher brokerage costs due to frequent buying/selling. | Low. Adjustments are only made when the composition of the tracked index changes. |

| Performance Fees | Some funds charge an additional percentage if they exceed a target return. | Non-existent. The objective is strictly replication. |

The impact of compound interest means that a 1.5% annual difference in fees causes a massive divergence in the final accumulated wealth after 20 or 30 years of investment.

Risk Assessment and Diversification

Risk is not measured solely by volatility (Beta), but by diversification and exposure to decision-making errors.

- Manager Risk (Active Management): There is an inherent risk that human decisions or the manager’s analytical models may be incorrect. However, during periods of severe market downturns (Bear Markets), an active manager theoretically has the flexibility to increase liquidity or rotate into defensive sectors to protect capital.

- Market Risk (Index Funds): By being obligated to track an index, passive funds suffer the full magnitude of market declines. However, they offer maximum diversification within their index (almost completely eliminating the specific risk of a single company) and remove the risk of human error in asset selection.

Frequently Asked Questions (FAQ)

Are index funds risk-free?

No. Index funds are subject to market risk. If the global index drops by 20%, the index fund will drop by approximately the same amount.

Which model is better in times of high inflation?

There is no single answer. Active management allows for the selection of companies with greater pricing power, while index funds tracking commodities or global markets offer structural protection by capturing the generalized movement of prices.

Can both strategies be combined?

Yes. In fact, the Core-Satellite strategy is widely used in corporate and wealth finance. It involves forming the core of the portfolio with low-cost index funds and using a small portion of the capital in active management to seek opportunities in specific niches.